Again, as noted above, all credit falls under one of four categories. Credit cards are the most numerous in the revolving credit world, and certainly the easiest to reach for as a remedy if you need to buy something online or on credit. Retail and gas cards, in particular, are relatively easy to qualify for and are often the first choice for consumers new to credit.

What are the different types of credit?

Or, if your only form of revolving credit is a credit card, you may want to open a small personal line of credit to demonstrate to lenders that you can handle different types of credit. As the name implies, credit mix represents the types of credit accounts you have in your credit report. When how does credit mix affect credit score you close a credit card, you can affect the length of your credit history and your credit utilization ratio. If the credit card is your only revolving credit, you may impact your credit mix as well. Credit mix is a term used to describe the different types of credit accounts you have.

How to improve your credit mix

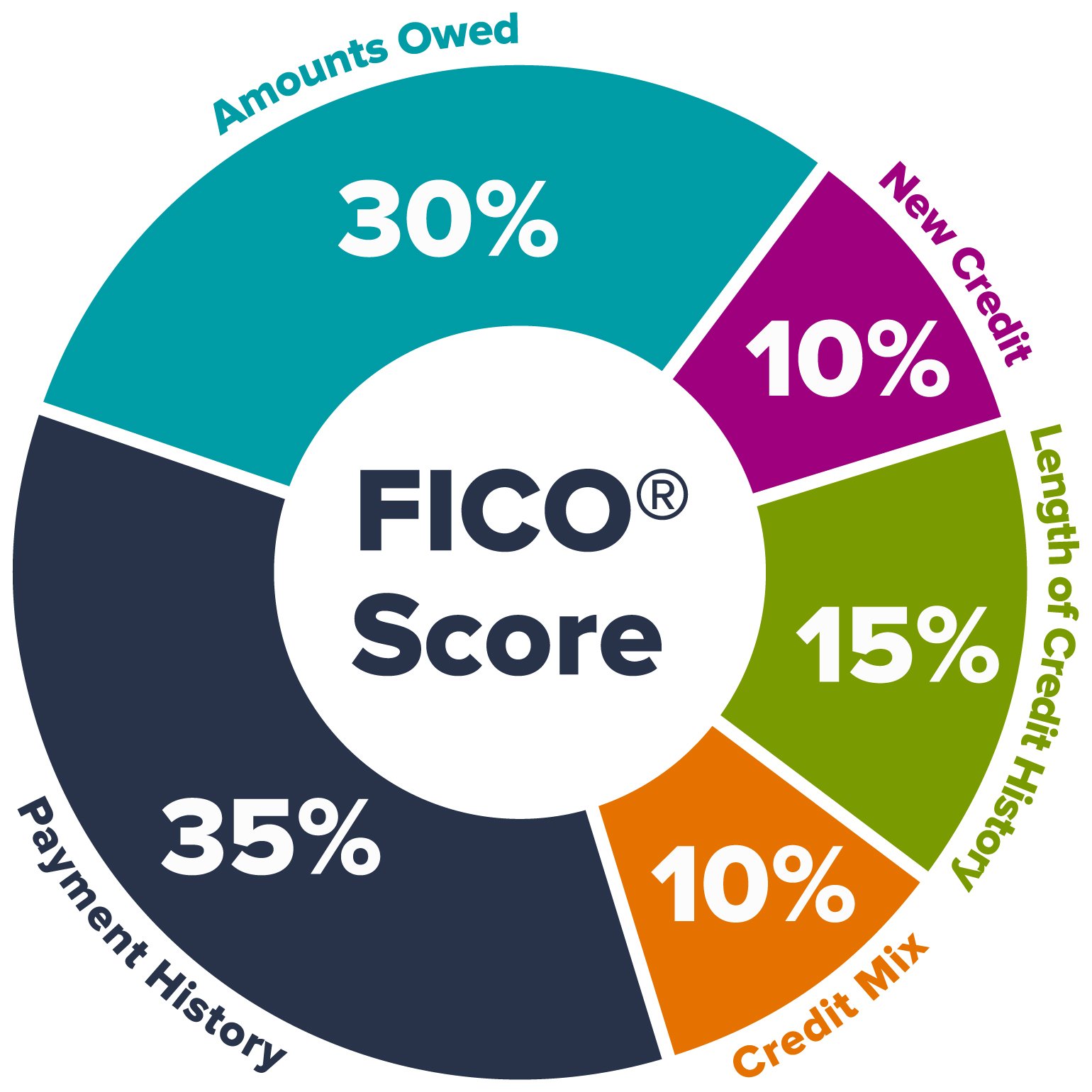

Your FICO Scores consider both positive and negative information in your credit report. The percentages in the chart reflect how important each of the categories is in determining how your FICO Scores are calculated. The importance of these categories may vary from one person to another—we’ll cover that in the next section. Our goal at FinMasters is to make every aspect of your financial life easier. We offer expert-driven advice and resources to help you earn, save and grow your money.

Bankrate logo

They focus on factors such as your payment history, your total debt, usage of available credit, length of credit history, credit mix and new credit. If you only have one or two revolving accounts open, closing one will definitely hurt your score. Closing one of your older accounts will reduce the length of your credit history and closing a credit card could raise your credit utilization rate. This type of credit has no fixed end date for the borrowing period and no set balance that must be paid monthly. Although you’ll need to make a minimum payment by the payment due date, you can pay more than the minimum, which affords payment flexibility.

- While it’s good to have a mix of different types of credit accounts, your credit mix likely won’t be the most important factor in determining your scores.

- Credit mix is a factor that tends to naturally evolve as you make financial moves throughout your life.

- Your credit score will benefit most when you have a healthy “mix” of both types, revolving and installment.

- Credit mix is one of the five factors that help determine your FICO® Score☉ , making up 10% of your score.

Note that closing accounts and paying off loans in full caps the payment history for those accounts, but it doesn’t immediately cancel out their ages for purposes of calculating length of credit history. Accounts you choose to close in good standing (meaning with no late payments) remain on your credit report for as long as 10 years. Keeping your debt levels low (especially credit card debt) and paying off your accounts on time are important steps you can take to help your credit scores. Maintaining good credit scores or building toward them isn’t just about credit mix; it’s also about managing your other credit-scoring factors, especially credit utilization ratio. FICO Scores will consider your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans. Revolving credit usually consists of credit cards but can include other types of revolving accounts like store credit lines, virtual credit cards, and a Home Equity Line of Credit or HELOC.

Million people in the U.S. do not have credit scores, which means they likely don’t have any form of credit account. The good news is that score damage from having high credit utilization can be reversed. Once you pay a high balance down and the creditor reports it to the credit bureaus, the damage disappears. Credit scoring companies calculate your scores from data in your credit reports. While they won’t reveal their exact formulas, they share the basic ingredients they use to calculate scores. Whether you’re building credit from scratch or rebuilding after some credit missteps, understanding the factors that go into your credit score can help you determine which steps to take.

For those looking to open a revolving credit account and have only a fair credit score, consider the Capital One Platinum Credit Card. This card is open to applicants with less-than-stellar credit ( Fair/Good) and comes with no annual fee nor foreign transaction fees for those traveling outside the U.S. If you have at least one credit card and a car payment and/or student loan in your name, you may be surprised to learn that you already have a good credit mix.

As long as you organize your finances and keep your accounts up to date, your score should improve over time. To avoid missed payments, have your payments come out of your bank account automatically. Think about what your financial goals are and how you intend to raise your credit score. For example, if you have insurmountable debt, opening a new credit account may not be a top priority. Instead, you should probably focus on paying down your debt, getting credit counseling using credit repair services, or consolidating your debt.

As you naturally open different credit accounts over time, a good credit mix can help you take your credit score into excellent territory. Your car payment or student loan, for which you make the same, fixed payment on each month, counts as installment credit. With this type of credit, you have a set balance divided out equally into a series of payments due each month until the specified end date. If you’re carrying high credit card debt, it’s better to focus on paying down those balances rather than investing in credit repair. Use any money you would spend on credit repair services to reduce debt instead. Focus your credit-building efforts on on-time payments and keeping balances low relative to credit limits, because those factors have the biggest effect on your scores.