At a contribution margin ratio of 80%, approximately $0.80 of each sales dollar generated by the sale of a Blue Jay Model is available to cover fixed expenses and contribute to profit. The contribution margin ratio for the birdbath implies that, for every $1 generated by the sale of a Blue Jay Model, they have $0.80 that contributes to fixed costs and profit. Thus, 20% of each sales dollar represents the variable cost of the item and 80% of the sales dollar is margin. Just as each product or service has its own contribution margin on a per unit basis, each has a unique contribution margin ratio. While contribution margin is expressed in a dollar amount, the contribution margin ratio is the value of a company’s sales minus its variable costs, expressed as a percentage of sales.

Contribution Margin Formula

The contribution margin is the foundation for break-even analysis used in the overall cost and sales price planning for products. More specifically, using contribution margin, your business can make new product journal entry for rent paid cash cheque advance examples decisions, properly price products, and discontinue selling unprofitable products that don’t at least cover variable costs. The business can also use its contribution margin analysis to set sales commissions.

Contribution Margin Ratio:

It also helps management understand which products and operations are profitable and which lines or departments need to be discontinued or closed. For example, raising prices increases contribution margin in the short term, but it could also lead to lower sales volume in the long run if buyers are unhappy about it. Before making any changes to your pricing or production processes, weigh the potential costs and benefits. Profit margin is calculated using all expenses that directly go into producing the product. It is the monetary value that each hour worked on a machine contributes to paying fixed costs.

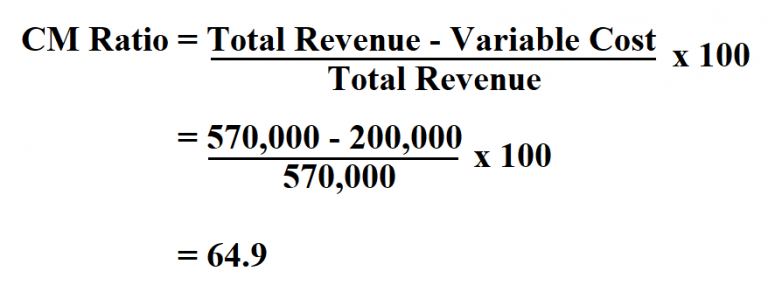

Contribution Margin Ratio

You work it out by dividing your contribution margin by the number of hours worked on any given machine. A subcategory of fixed costs is overhead costs that are allocated in GAAP accounting to inventory and cost of goods sold. This allocation of fixed overhead isn’t done for internal analysis of contribution margin. When the contribution margin is calculated on a per-unit basis, it is referred to as the contribution margin per unit or unit contribution margin.

Business Cards

You can use contribution margin to help you make intelligent business decisions, especially concerning the kinds of products you make and how you price those products. Imagine that you have a machine that creates new cups, and it costs $20,000. To make a new cup, you have to spend $2 for the raw materials, like ceramics, and electricity to power the machine and labor to make each product. This is because fee-for-service hospitals have a positive contribution margin for almost all elective cases mostly due to a large percentage of OR costs being fixed. For USA hospitals not on a fixed annual budget, contribution margin per OR hour averages one to two thousand USD per OR hour. However, when CM is expressed as a ratio or as a percentage of sales, it provides a sound alternative to the profit ratio.

- If all variable and fixed costs are covered by the selling price, the breakeven point is reached, and any remaining amount is profit.

- Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others.

- The contribution margin can be presented in dollars or as a percentage.

Contribution Margin: What Is It and How To Calculate It

11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links. Next, the CM ratio can be calculated by dividing the amount from the prior step by the price per unit. The 60% CM ratio implies the contribution margin for each dollar of revenue generated is $0.60. The greater the contribution margin (CM) of each product, the more profitable the company is going to be, with more cash available to meet other expenses — all else being equal. This metric is typically used to calculate the break even point of a production process and set the pricing of a product. They also use this to forecast the profits of the budgeted production numbers after the prices have been set.

This, in turn, can help people make better decisions regarding product & service pricing, product lines, and sales commissions or bonuses. Let’s say we have a company that produces 100,000 units of a product, sells them at $12 per unit, and has a variable costs of $8 per unit. The formula to calculate the contribution margin is equal to revenue minus variable costs. Management uses the contribution margin in several different forms to production and pricing decisions within the business. This concept is especially helpful to management in calculating the breakeven point for a department or a product line. Management uses this metric to understand what price they are able to charge for a product without losing money as production increases and scale continues.

Very low or negative contribution margin values indicate economically nonviable products whose manufacturing and sales eat up a large portion of the revenues. Investors examine contribution margins to determine if a company is using its revenue effectively. A high contribution margin indicates that a company tends to bring in more money than it spends. Investors and analysts may also attempt to calculate the contribution margin figure for a company’s blockbuster products. For instance, a beverage company may have 15 different products but the bulk of its profits may come from one specific beverage.